First of all, the CNMI, like every US state, has laws that shield your income from creditors so that you can provide for your basic needs. Even if you lost in court and a judgment was issued against you for a consumer debt, you can still keep what you need for the essentials. For low-income people, this exemption can end up protecting all of the income. This is called being “judgment proof.”

In the CNMI, not many know of this right. In court, they end up agreeing to pay something back on a regular basis, even if they can’t afford it. If the debtor agrees, the court swiftly issues an order to pay. Oftentimes, the debtor feels compelled to agree to something. Anything, actually.

The federal government also established a minimum amount of what can be garnished from your paycheck. This was done in 1968 with the passing of of the Consumer Credit Protection Act, another one of LBJ's Great Society initiatives. States can’t dip below the minimum protection, but are free to add more to it.

Keep in mind that the federal garnishment restrictions were not only meant to safeguard the poor. Congress considered it a way to prevent imprudent extensions of credit. The act was designed to encourage good industry practice.

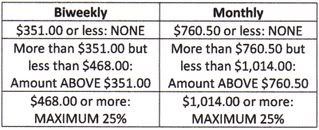

One crucial difference between CNMI law and federal law is that the federal law provides a formula to determine the garnishment ceiling. The formula is based on the federal minimum wage, which is currently set at $5.85/hr. (with 70 cent increases annually until 2009, when the $7.25/hr. mark is reached). The limit of what can be garnished is the lesser of ) 25% of disposable weekly earnings or 2) any amount over 30 times the federal minimum hourly wage. Yes, I can’t visualize that too, so here’s another way to look at what can be taken when your biweekly or monthly paycheck is in the following ranges:

(taken from US DoL fact sheet)

The CNMI does not have a formula. Here, a court is required to decide on a case-by-case basis what income is needed for the reasonable living requirements of the debtor and the dependents. As I mentioned, with the Superior Court dealing with so many cases and the need for judicial efficiency, what happens (when the debtor doesn't have an attorney) is that some haggling is done, and a debtor agrees to something. What is lost in the shuffle is that the debtor is never given a chance to exercise the right to not pay.

Our appeal currently before the CNMI Supreme Court on this issue is Triple J v. Mateo Norita, et al., CV-06-0031-GA. There are several legal arguments Triple J lays out on why the federal law should not apply in the CNMI. For example, the Consumer Credit Protection Act requires state and federal courts to abide by the wage garnishment limit. However, “state” isn’t defined at all for these purposes. And, as the argument goes, the CNMI isn't a state. This may end the question, but every persuasive source out there is inclined to include the CNMI, such as the US Dept. of Labor and the Northern Marianas Commission on Federal Laws. Despite the difference between the minimum wage here and in the US, The Commission believed the formula should apply here for the following reason: “...the obvious intent [of the federal limit] is to allow the employee to retain enough earnings to purchase the necessities of life: food, shelter, and so forth. While earnings in the Northern Mariana Islands are generally less than in other parts of the United States, there is no evidence that the costs of necessities are also less.”

Instead of bogging down this post on all the other legal issues, I thought I’d at least bring the topic out of the courthouse and let others get a feel on where they stand. (Judges have been known to make up their mind first based on social, moral and practical grounds, then figure out the legal basis next.)

Our position is with the findings of the NMI Commission. The CNMI should be no different when it comes to protecting its people. The risks of extending credit should be fairly spread out. Creditors shouldn't have more advantages in the CNMI than anywhere else in the US.

No comments:

Post a Comment