The Marianas Office is sad to say that our front-office secretary, Polly Anne Sablan, has resigned (effective the end of the month). Like many others in our community, she is moving to the mainland U.S. to try for a better opportunity for herself and her children.

We are accepting applications to fill her position as LEGAL SECRETARY.

Qualifications include, but are not necessarily limited to, the following:

1. Must have high school or better education.

2. Need to have good speaking and writing skills.

3. You must have your own transportation and a valid CNMI driver's license.

4. We prefer fluency in Chamorro or Carolinian, or both.

Job duties include, but are not limited to, the following:

1. reception (answering the telephone, greeting applicants, clients and other members of the general public who come to the office).

2. secretarial work (filing, typing, copying, etc.)

3. client communication (interviewing, taking and relaying messages and advice, writing letters, etc.)

4. field work (service of legal process, tracking down documents, witnesses, etc., delivering and picking up documents and other things, some banking, etc.)

MLSC is an equal employment opportunity employer. MLSC offers medical, dental and optical benefits. Salary depends on experience.

Applications are available at our office in Civic Center, Susupe.

Wednesday, November 28, 2007

Wednesday, November 21, 2007

Supreme Court Decides Against Debtors

Last week, the CNMI Supreme Court issued its decision in Triple J Saipan v. Mateo V. Norita et al. The court ruled that federal law limiting how much can be garnished from your wages does not apply in the CNMI. We unsuccessfully argued that the federal law not only applies here, but that it also 1) offers more protections to debtors and 2) more fairly spreads out the risks of credit extension between creditors and debtors.

What the Supreme Court decision means is that the status quo is maintained. Our courts turn to local law when figuring out a debtor’s schedule to pay back a debt. In practice, as I discussed in my previous post of 11/1/07, there is an uneven playing field. Low-income debtors who can’t afford an attorney end up paying something back on a regular basis, even though their income is considerably below poverty level. This will continue to happen despite the fact that debtors have the right to keep everything they need for their basic needs.

Our clients’ household income was SSI and the minimum wage (then $3.05/hour). SSI (or Supplemental Security Income), is a federal benefit entitled to those who are poor and disabled. They have already been deemed poor enough to receive SSI. Those benefits were not an issue in the case, because they cannot be taken to pay back a debt. That’s a federal law that unquestionably applies in the CNMI. On the other hand, the court endorsed a payment order against the minimum wage earner.

Today, the minimum wage in the CNMI is $3.55/hour. This comes to a gross annual income of $7,384. Under the 2007 federal poverty guidelines, the threshold amount for a household of one is $10,210 per year. Those of us living in poverty here are less protected from creditors than elsewhere in the States. This is the court's implicit opinion.

In reaching its decision, the court made a difference between a garnishment and an “order in aid of judgment,” which is the typical CNMI court order that requires a debtor to regularly surrender money to the creditor as each paycheck is received. As the court argues, a garnishment is when you take money from a third party who owes the debtor, such as the debtor’s employer. Technically then, taking money directly from the debtor is not a garnishment. Since the federal law governs garnishments, it has no bearing on our orders in aid of judgment.

What the court completely fails to take into account is that a garnishment and an order in aid of judgment have the same effect: you risk being deprived of future paychecks needed to support yourself and your family. What good is a paycheck when you have to surrender it the second you receive it?

Thursday, November 1, 2007

Federal Law on Debtor Relief in the CNMI

In our previous post on 9/13/07, we provided an introduction to debt collection and your rights as a debtor. One of our pending Commonwealth Supreme Court cases is dealing with what it means to be “judgment proof.” The case turns on the question of whether federal law on garnishment restrictions applies here. We say it does.

First of all, the CNMI, like every US state, has laws that shield your income from creditors so that you can provide for your basic needs. Even if you lost in court and a judgment was issued against you for a consumer debt, you can still keep what you need for the essentials. For low-income people, this exemption can end up protecting all of the income. This is called being “judgment proof.”

In the CNMI, not many know of this right. In court, they end up agreeing to pay something back on a regular basis, even if they can’t afford it. If the debtor agrees, the court swiftly issues an order to pay. Oftentimes, the debtor feels compelled to agree to something. Anything, actually.

The federal government also established a minimum amount of what can be garnished from your paycheck. This was done in 1968 with the passing of of the Consumer Credit Protection Act, another one of LBJ's Great Society initiatives. States can’t dip below the minimum protection, but are free to add more to it.

Keep in mind that the federal garnishment restrictions were not only meant to safeguard the poor. Congress considered it a way to prevent imprudent extensions of credit. The act was designed to encourage good industry practice.

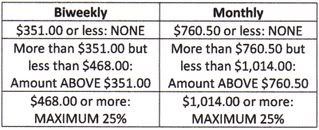

One crucial difference between CNMI law and federal law is that the federal law provides a formula to determine the garnishment ceiling. The formula is based on the federal minimum wage, which is currently set at $5.85/hr. (with 70 cent increases annually until 2009, when the $7.25/hr. mark is reached). The limit of what can be garnished is the lesser of ) 25% of disposable weekly earnings or 2) any amount over 30 times the federal minimum hourly wage. Yes, I can’t visualize that too, so here’s another way to look at what can be taken when your biweekly or monthly paycheck is in the following ranges:

(taken from US DoL fact sheet)

The CNMI does not have a formula. Here, a court is required to decide on a case-by-case basis what income is needed for the reasonable living requirements of the debtor and the dependents. As I mentioned, with the Superior Court dealing with so many cases and the need for judicial efficiency, what happens (when the debtor doesn't have an attorney) is that some haggling is done, and a debtor agrees to something. What is lost in the shuffle is that the debtor is never given a chance to exercise the right to not pay.

Our appeal currently before the CNMI Supreme Court on this issue is Triple J v. Mateo Norita, et al., CV-06-0031-GA. There are several legal arguments Triple J lays out on why the federal law should not apply in the CNMI. For example, the Consumer Credit Protection Act requires state and federal courts to abide by the wage garnishment limit. However, “state” isn’t defined at all for these purposes. And, as the argument goes, the CNMI isn't a state. This may end the question, but every persuasive source out there is inclined to include the CNMI, such as the US Dept. of Labor and the Northern Marianas Commission on Federal Laws. Despite the difference between the minimum wage here and in the US, The Commission believed the formula should apply here for the following reason: “...the obvious intent [of the federal limit] is to allow the employee to retain enough earnings to purchase the necessities of life: food, shelter, and so forth. While earnings in the Northern Mariana Islands are generally less than in other parts of the United States, there is no evidence that the costs of necessities are also less.”

Instead of bogging down this post on all the other legal issues, I thought I’d at least bring the topic out of the courthouse and let others get a feel on where they stand. (Judges have been known to make up their mind first based on social, moral and practical grounds, then figure out the legal basis next.)

Our position is with the findings of the NMI Commission. The CNMI should be no different when it comes to protecting its people. The risks of extending credit should be fairly spread out. Creditors shouldn't have more advantages in the CNMI than anywhere else in the US.

First of all, the CNMI, like every US state, has laws that shield your income from creditors so that you can provide for your basic needs. Even if you lost in court and a judgment was issued against you for a consumer debt, you can still keep what you need for the essentials. For low-income people, this exemption can end up protecting all of the income. This is called being “judgment proof.”

In the CNMI, not many know of this right. In court, they end up agreeing to pay something back on a regular basis, even if they can’t afford it. If the debtor agrees, the court swiftly issues an order to pay. Oftentimes, the debtor feels compelled to agree to something. Anything, actually.

The federal government also established a minimum amount of what can be garnished from your paycheck. This was done in 1968 with the passing of of the Consumer Credit Protection Act, another one of LBJ's Great Society initiatives. States can’t dip below the minimum protection, but are free to add more to it.

Keep in mind that the federal garnishment restrictions were not only meant to safeguard the poor. Congress considered it a way to prevent imprudent extensions of credit. The act was designed to encourage good industry practice.

One crucial difference between CNMI law and federal law is that the federal law provides a formula to determine the garnishment ceiling. The formula is based on the federal minimum wage, which is currently set at $5.85/hr. (with 70 cent increases annually until 2009, when the $7.25/hr. mark is reached). The limit of what can be garnished is the lesser of ) 25% of disposable weekly earnings or 2) any amount over 30 times the federal minimum hourly wage. Yes, I can’t visualize that too, so here’s another way to look at what can be taken when your biweekly or monthly paycheck is in the following ranges:

(taken from US DoL fact sheet)

The CNMI does not have a formula. Here, a court is required to decide on a case-by-case basis what income is needed for the reasonable living requirements of the debtor and the dependents. As I mentioned, with the Superior Court dealing with so many cases and the need for judicial efficiency, what happens (when the debtor doesn't have an attorney) is that some haggling is done, and a debtor agrees to something. What is lost in the shuffle is that the debtor is never given a chance to exercise the right to not pay.

Our appeal currently before the CNMI Supreme Court on this issue is Triple J v. Mateo Norita, et al., CV-06-0031-GA. There are several legal arguments Triple J lays out on why the federal law should not apply in the CNMI. For example, the Consumer Credit Protection Act requires state and federal courts to abide by the wage garnishment limit. However, “state” isn’t defined at all for these purposes. And, as the argument goes, the CNMI isn't a state. This may end the question, but every persuasive source out there is inclined to include the CNMI, such as the US Dept. of Labor and the Northern Marianas Commission on Federal Laws. Despite the difference between the minimum wage here and in the US, The Commission believed the formula should apply here for the following reason: “...the obvious intent [of the federal limit] is to allow the employee to retain enough earnings to purchase the necessities of life: food, shelter, and so forth. While earnings in the Northern Mariana Islands are generally less than in other parts of the United States, there is no evidence that the costs of necessities are also less.”

Instead of bogging down this post on all the other legal issues, I thought I’d at least bring the topic out of the courthouse and let others get a feel on where they stand. (Judges have been known to make up their mind first based on social, moral and practical grounds, then figure out the legal basis next.)

Our position is with the findings of the NMI Commission. The CNMI should be no different when it comes to protecting its people. The risks of extending credit should be fairly spread out. Creditors shouldn't have more advantages in the CNMI than anywhere else in the US.

Subscribe to:

Comments (Atom)